Bullion Banks Have “No Way Out” From Big Gold Shorts

August 8, 2020 in News by RBN Staff

Source: www.zerohedge.com

by Tyler Durden

Authored by Alasdair Macleod via GoldMoney.com,

There appears to be no way out for the bullion banks deteriorating $53bn short gold futures positions ($38bn net) on Comex. An earlier attempt between January and March to regain control over paper gold markets has backfired on the bullion banks.

Unallocated gold account holders with LBMA member banks will shortly discover that that market is trading on vapour. According to the Bank for International Settlements, at the end of last year LBMA gold positions, the vast majority being unallocated, totalled $512bn — the London Mythical Bullion Market is a more appropriate description for the surprise to come.

An awful lot of gold bulls are going to be disappointed when their unallocated bullion bank holdings turn to dust in the coming months — perhaps it’s a matter of a few weeks, perhaps only days — and synthetic ETFs will also blow up. The systemic demolition of paper gold and silver markets is a predictable catastrophe in the course of the collapse of fiat money’s purchasing power, for which the evidence is mounting. It is set to drive gold and silver much higher, or more correctly put, fiat currencies much lower.

This is only the initial catalysing phase in the rapidly approaching death of fiat currencies.

Introduction

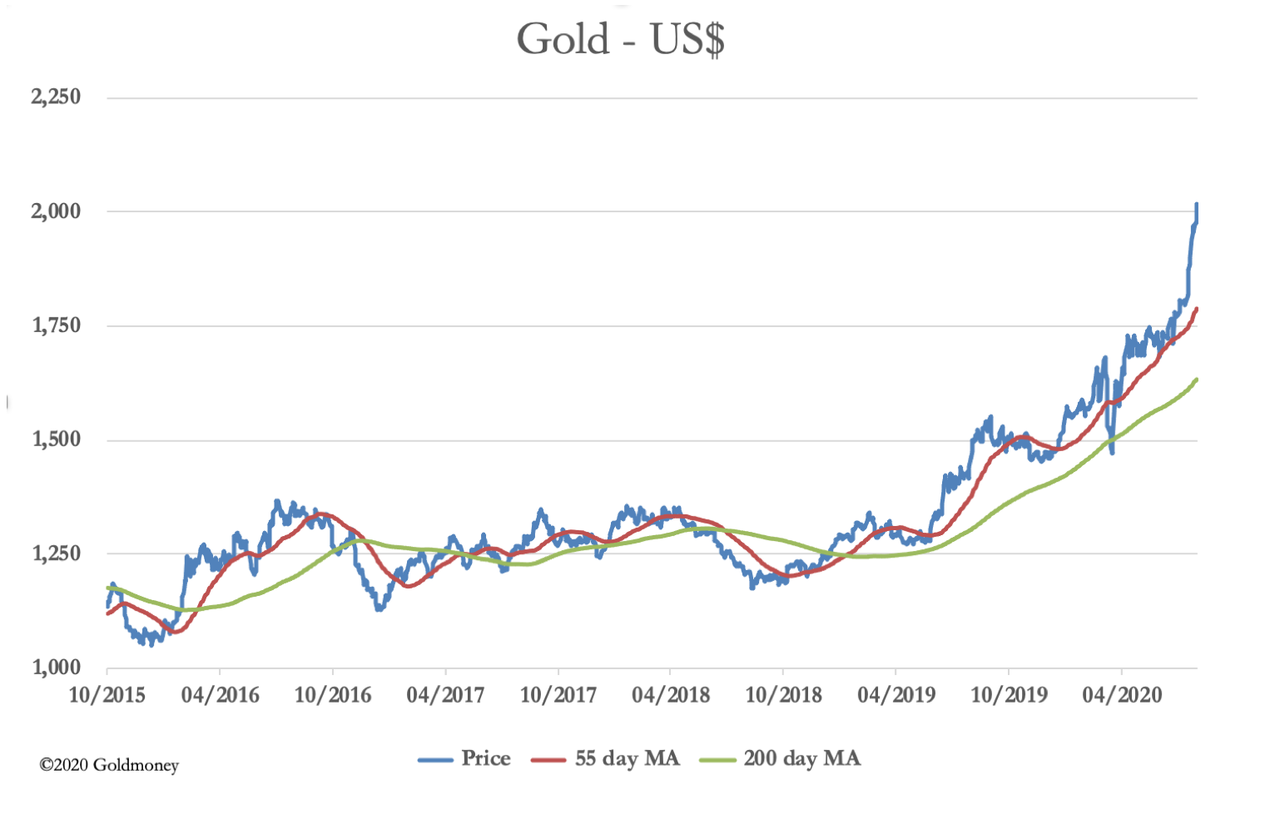

Measured in dollars, the current bull market for gold started in December 2015, since when the price in dollars has almost doubled. Other than the odd headline when gold exceeded its previous September 2011 high of $1920, only gold bugs seem to be excited. But in our modern macroeconomic world of government-issued currencies, which has moved on from the days when gold operated as a monetary standard, it is viewed as an anachronism; a pet rock, as Jason Zweig of the Wall Street Journal called it in 2015, only a few months before this bull market commenced.

Despite almost doubling, Zweig’s view of gold is still mainstream. His comment follows the spirit of today’s macroeconomic hero, John Maynard Keynes, who called the gold standard a barbaric relic in his 1924 Tract on Monetary Reform. Keynes went on to invent macroeconomics on the back of his 1936 General Theory, and whether you profess to be Keynesian or not, as an investor you will almost certainly kowtow to macroeconomics. It has been well-nigh impossible to have a successful career in the investment industry unless you subscribed to inflationist Keynesian theories. You are required to substitute the economics of aggregates for those of the human action of individuals, upon which classical economics was based. And with it, you must unquestionably accept the state theory of money.

Well, we are now witnessing the cataclysmic ending of the Keynesian fallacy; the destruction of macroeconomics in a systemic failure centred on paper markets for gold and silver.

The rescue attempt has already failed

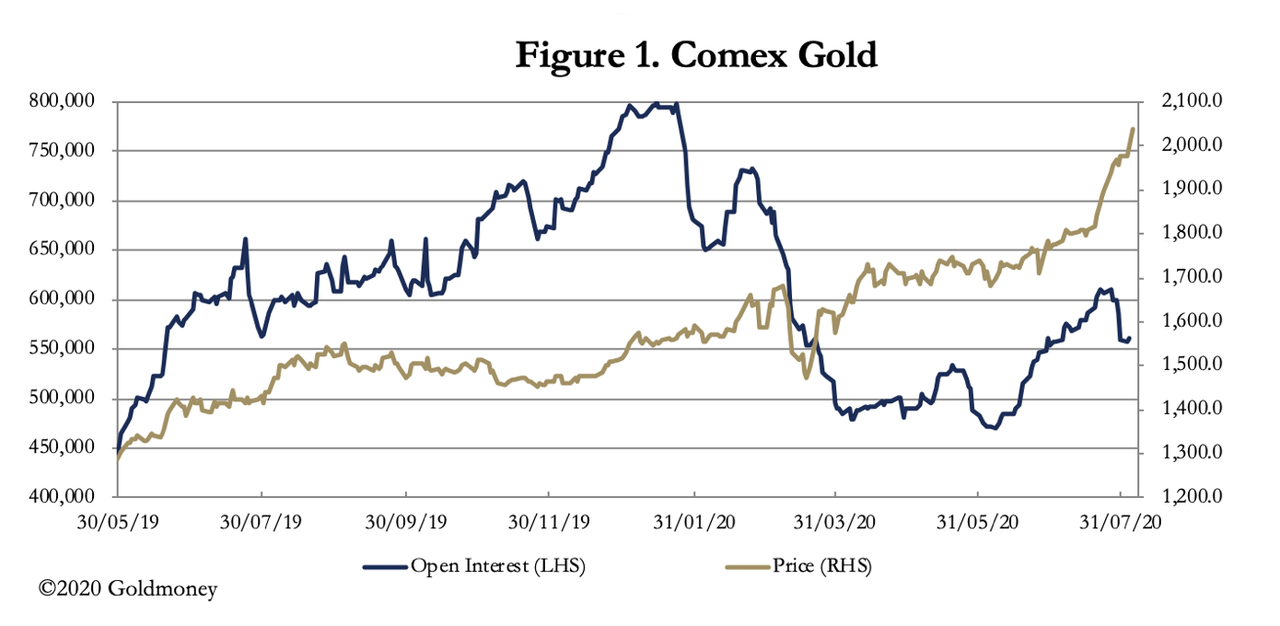

You may have missed the establishment’s last-ditch attempt earlier this year to save itself. Figure 1 below shows its failure.

Comex open interest peaked in January, when the gold contract was being overwhelmed by global demand. Never before had open interest been this high: the previous all-time record had been in July 2016, when it hit 658,000 contracts. At that time, the market had recovered strongly from a deeply oversold condition, the price rallying from the December low in our headline chart, from $1049 to $1380. That was successfully crushed with open interest taken down to 392,000 and the gold price to $1120. However, the take-down which commenced in earnest in January this year did not succeed.

There is no question it was a coordinated attempt by the bullion bank establishment to contain a developing crisis. From its peak of 799,541 contracts on 15 January open interest fell to 553,030 on 23 March. Initially, the gold price continued rising to $1680 on 9 March, but by 18 March it finally reacted, falling to $1471 in only nine trading sessions. But while open interest went on to fall to 470,000 in early-June, the price exploded higher with unprecedented price premiums developing on Comex from 23 March onwards. The bullion banks’ short exposure net of longs on Comex in a rising market had risen to $35bn and the gross position was $53.5bn before the attempt to drive the market lower. Today, the respective figures are $38.3 and $53bn.

The failure of this well-worn tactic precludes it from being used again. We look at the seriousness of the current position on Comex and the LBMA later in this article.