Goldman Trading Desk: “$13 Billion Of Demand Every Day… That’s The Line That Will Hit The Press”

August 11, 2022 in News by RBN Staff

Source: ZeroHedge.com

While reading today’s end-of-day market recap from Bloomberg titled “Cut-to-Bone Positioning Set the Stage for Stocks’ Big Bounce” we couldn’t help but laugh at how the author frames the massive melt up that started in June, accelerated mid-July and really took off in late July and early August, by saying that “nobody saw it coming, and now everyone wants in.” Well, actually, maybe readers of Bloomberg didn’t, but our subs did:

- Funds Furious As Powell Pours Gasoline On “Most Hated Rally”, Forcing Panic Buying (July 28)

- Massive CTA Demand Coming In (July 10)

- Buyback Blackout Period Is Over, And 10 More Reasons Why Goldman Calls The End Of The Market Carnage (May 2)

- “Will Retail Traders Force Institutions To Chase Stocks” (April 4)

But while Bloomberg will be doing more meaningless post-mortems in a few weeks explaining after the fact “how an improbable equity market bounce is threatening to become a meltup“, our readers will again be ahead of the curve in what comes next courtesy of the most comprehensive flow of funds and positional analysis from the Goldman Sales and Trading desk (which unlike the bank’s sellside research, has actually been spot on in their calls so far this week).

No recession they say…

…but the 2/10 year spread seems to think otherwise. New low and the gap vs SPX getting very wide.

Source: Refinitiv

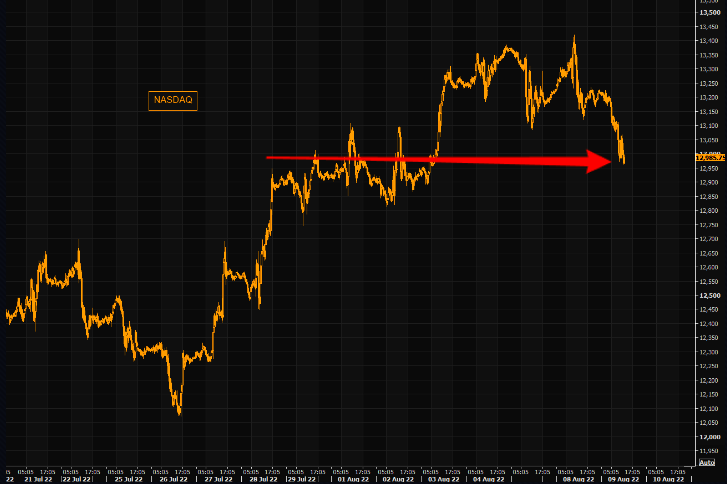

Perceived vs realized bull

Everybody is in full bullish mode, but NASDAQ is trading at the same levels we traded at 7-8 sessions ago.

Source: Refinitiv

As SOX goes…

so goes the market, or?

Source: Refinitiv

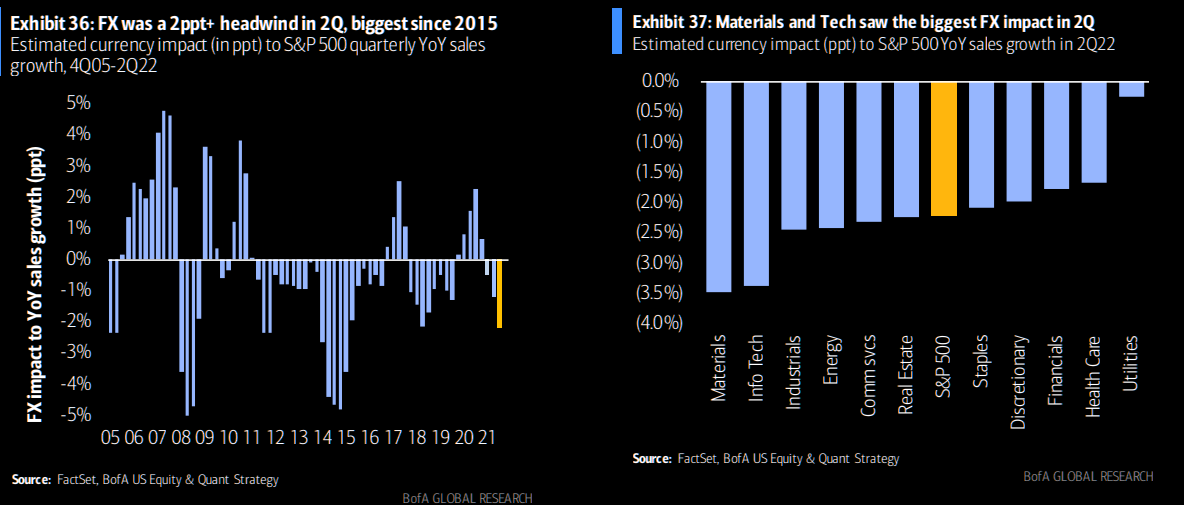

The dollar is starting to hurt

Biggest losers from the strong dollar is tech and materials. BofA reminds us: “…a 13% YoY rise in the USD translated to a 2ppt headwind to sales growth, the biggest hit since 2015”. Does this become a topic soon?

Source: BofA

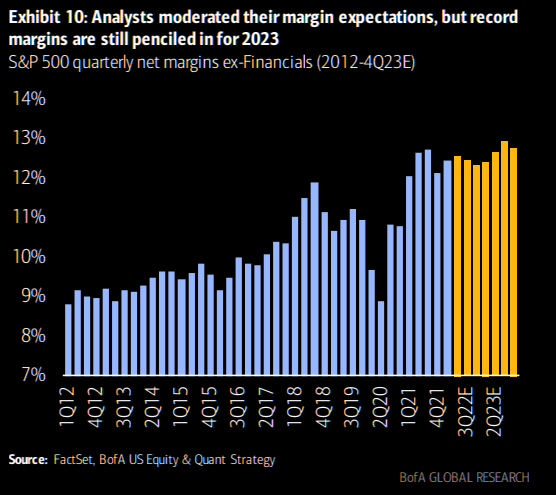

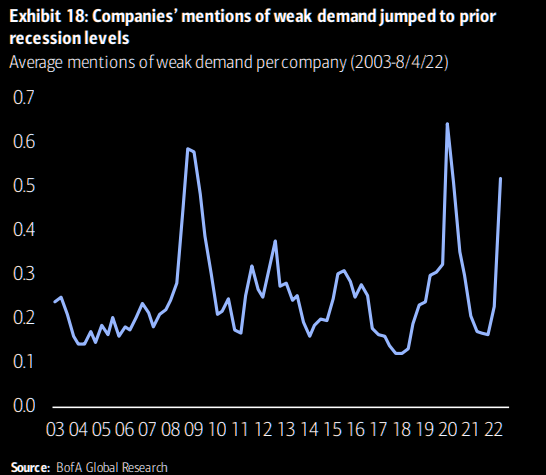

No bear in margins

Analysts are still projecting record margins for 2023. What happened to weakening demand? Second chart shows companies’ mentions of weak demand. Go figure…

Source: BofA

Source: BofA

Time for energy (again)?

JPM asks themselves if it is time to reconsider going long energy? A few bullets:

1. Energy demand proved to be more resilient than expected, with recovery underway

2. while S&P 500 has a -1.7% revision in FY22 earnings growth comparing with July 1, 2022, Energy has the highest positive revision of +20.9% relative to July 1, 2022

3. recent under performance of the energy driven by the falling risk premium due to global energy demand destruction, caused by higher recession risks…but the investment bank sees demand being resilient…

4. Even for recessionary years, the demand destruction has been limited

5. Russia remains a wild card

Source: JPM/Bloomberg

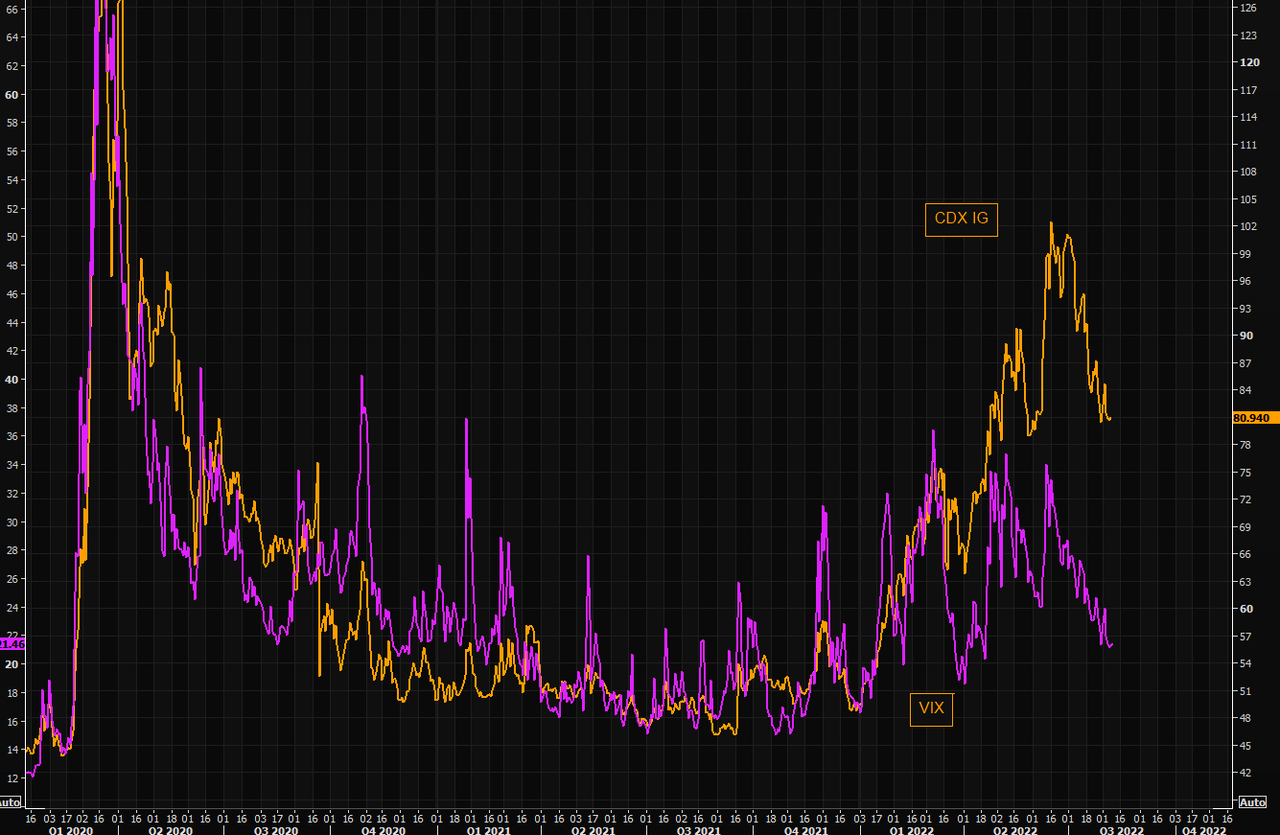

Things have calmed down

Both VIX and US credit protection, CDX IG, have come down over past weeks. US credit protection never reached the same panic as we saw in Europe, but it also remains elevated. The question is if calm is followed by calm…?

Source: Refinitiv

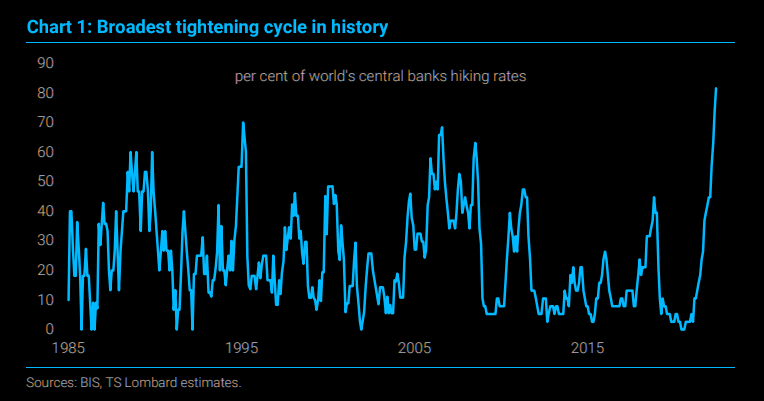

Never forget – tightening bonanza is huge

Few bullets via TS Lomabrd:

1. Central bankers can no longer guide market rate expectations

2. Beyond neutral, further policy tightening depends on data outturns

3. Bond markets signal a policy error, but the authorities seem unperturbed

Source: TS Lombard

Cash at record highs

Long-only mutual fund cash holdings (from an absolute $ perspective) remain near record highs (>$200b), as per GS data. This adds to the tsunami of “sentiment & positioning” indicators that scream “further squeeze”. Two or three more of these indicators that now are being super-well flagged from sell-side and it is probably time to short again….

Time for some downside action again?

This time is different, but what if we are to follow the autumn of 2008? The analogy isn’t as perfect, but could come into play, at least partly…

Source: Refinitiv