It’s A “Defund-The-Global-Police” Moment, Jen Says De-Dollarization Is Happening At A “Stunning” Pace

April 24, 2023 in News by RBN Staff

source: zerohedge

BY TYLER DURDEN

Over the last few weeks, it has seemed you can’t turn a page, blink at a pixel, or hear a news report without some form of de-dollarization headline shrieking at you. From Brazil to Saudi Arabia, and from India to Argentina, and increasing number of nations are ‘reportedly’ shifting away from the dollar hegemon.

Some recent headlines:

- “No Reason” For Malaysia To Rely On US Dollar, PM Warns As Yuan Influence Grows

- De-Dollarization Just Got Real

- Here Are 7 Signs That Global De-Dollarization Has Just Shifted Into Overdrive

- De-Dollarization Has Begun

Eyeballing the Dollar Index (or some other broad index of fiat relativity) drops modest hints but the nature of the relationship of one un-backed currency against another makes that comparison worthless in the longer-term.

But below the surface, the dollar’s fecal matter is striking rotating objects at an increasing pace and Stephen Jen – infamous for his coining of the ‘dollar smile’ while at Morgan Stanley which posits that the US Dollar tends to do well when the economy is soaring or slumping – recently quantified just how rapidly the de-dollarization is ocurring.

Jen, who now runs money at Eurizon SLJ, warned in a recent briefing note, that the dollar is losing its reserve status at a faster pace than generally accepted, as many analysts have failed to account for last year’s frantic swings in exchange rates.

“The dollar suffered a stunning collapse in 2022 in its market share as a reserve currency, presumably due to its muscular use of sanctions,” Jen and his colleague Joana Freire wrote.

“Exceptional actions taken by the US and its allies against Russia have startled large reserve-holding countries,” most of which are emerging economies from the so-called Global South, they said.

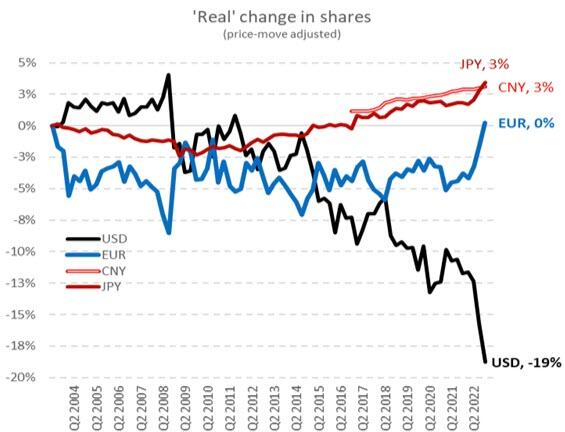

As The FT reports, Jen estimates that if you adjust for price changes the dollar’s share of official global reserve currencies has gone from about 73 per cent in 2001 to around 55 per cent in 2021.

Then, last year, it fell to 47 percent of total global reserves.

Source: Eurizon SLJ Capital

Jen and Freire go on to ominously explain that the USD is losing its market share as a reserve currency at a much faster rate than is commonly believed.

“After steady declines in its global market share for the past two decades, in 2022 the dollar lost market share at a pace 10 times as rapidly. Analysts have failed to detect this big change because they calculate the nominal value of the world’s central banks’ dollar holdings without considering the changes in the price of the dollar. Adjusting for these price changes, the dollar, we calculate, has lost some 11 percent of its market share since 2016 and double that amount since 2008.

This erosion in the USD’s reserve currency status has accelerated precipitously since the start of the war in Ukraine. Exceptional actions taken by the US and its allies against Russia have startled large reserve-holding countries, most of which are from the Global South.

…Without the need for us to take sides in this debate on Ukraine, it seems reasonable to speculate that the main driver of the collapse in USD’s reserve status in 2022 may have reflected a panicked reaction to property rights being jeopardised. What we witnessed in 2022 was sort of a ‘defund-the-global-police’ moment, whereby many reserve managers in the world disagreed with the conduct of both Russia and the US.”

This is suddenly serious, as Jen and Freire argue that “The prevailing view of ‘nothing-to-see-here’ on the US dollar as a reserve currency seems too innocuous and complacent.”

“What needs to be appreciated by investors is that, while the Global South is unable to totally avoid using the dollar, much of it has already become unwilling to do so.”

The greenback’s share in global reserves slid last year at 10 times the average speed of the past two decades as a number of countries looked for alternatives after Russia’s invasion of Ukraine triggered sanctions.

Moreover, as Jen stresses, there are actually two pillars that make the US dollar so mighty: its role as the reserve currency of choice, and its dominant use in global finance and trade. “Investors ought not be confused by these two different concepts,” he argues.

“While the Global South seems unwilling to continue to hold dollar assets, they do not seem to have the ability to divest from the US dollar as an international currency, particularly for financial transactions.

We suspect it will be very difficult to overcome the strong network effects that have been behind the dollar’s international currency status.

The key to topple the dollar’s throne as an international currency is predicated on the relative developments and stability in the various financial markets. If the financial markets outside the US could thrive (growing in size and becoming ever more energetic, without being unstable), and if the opposite happens in the US, the dollar could very well meet its demise.

This is, however, not an imminent risk, in our opinion, though the trends are heading in that direction.“

Still think it won’t or can’t happen, here’s George Soros… from 2009…

[ JOIN US ] I am making a good salary from home 16580-47065/ Doller week , which is amazing under a year ago I was jobless in a horrible economy. I thank God every day I was blessed with these instructions and now it’s my duty to pay it forward and share it with Everyone,

Here is I started.…………> http://www.jobsrevenue.com

[ JOIN US ] I am making a good salary from home 16580-47065/ Doller week , which is amazing under a year ago I was jobless in a horrible economy. I thank God every day I was blessed with these instructions and now it’s my duty to pay it forward and share it with Everyone,

Here is I started.…………> http://www.jobsrevenue.com