The Fed Blows Biggest Bond Bubble Ever: March IG Bond Issuance Hits $271BN, An Absolute Record

April 1, 2020 in News by RBN Staff

Source: Zero Hedge by Tyler Durden

When the Fed broke the last frontier of moral hazard – at least until it starts openly purchasing ETFs and single stocks after the next market crash, thereby fully nationalizing the market – and announced it, or rather Blackrock, would not only expand its QE to “unlimited” but also buy investment grade bonds and the IG ETF, LQD, it effectively tore the bond market into two categories: that backstopped by the Fed, and that which isn’t (something we described in “Bond Market Tears In Two: Distressed Debt Is Cratering, As Fed Buying Of Investment Grade Sends LQD NAV Soaring“).

It also unleashed the biggest debt bubble of all time.

Why? Because by explicitly guaranteeing investment grade debt, the Fed – by making BBB and higher rated debt effectively risk-free – not only precipitated the biggest one-day surge and inflow into LQD, but unleashed an unprecedented free for all as every single investment grade company – especially those soon to be fallen angels who will be downgraded to junk – have rushed into the bond market to issue debt and raise cash while they can at artificially low yields.

And the data confirms it: according to BofA, after the IG market was largely shut down in the two weeks ahead of the Fed’s March 23 bond buying announcement, US new issuance reached a new monthly record of $260.7 billion in March 2020, bringing YtD to $509.7 billion – the fastest ever start to a year and 47% ahead of 2019’s pace.

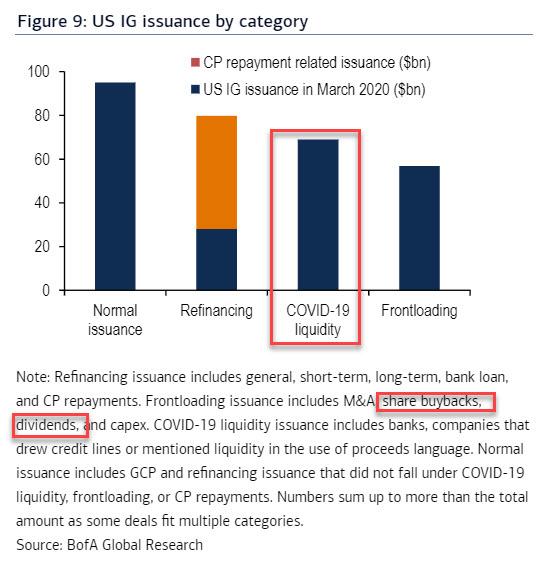

Looking at the use of proceeds, BofA observes that refinancings continued at a strong $79.8bn, but as the commercial paper market froze $51.8bn was specifically earmarked for terming that out. In addition, there was roughly $69bn of COVID-19 liquidity-related issuance from banks and companies that drew credit lines or mentioned liquidity in the use of proceeds language. What is more remarkable is that is that another $57bn was for frontloaded issuance for capex, M&A as well as – drumroll – share buybacks and dividends.

Yes, even at this moment, having seen the Boeing blowback which repurchased over $50BN in stock pushing its debt load to record highs and now demands a $60BN bailout, companies have the gall to issue debt and buyback stock! Something tells us there will be a lot of angry articles in the NYT singling out each and every one of those companies, especially if they have or plan to fire even one single worker.

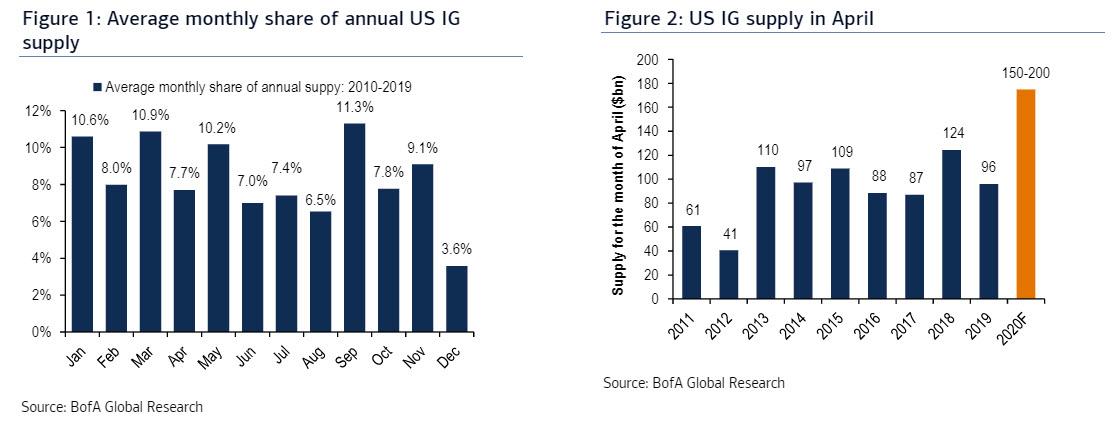

And it’s just starting. Looking ahead, BofA notes that April is seasonally a lighter month than March in primary, accounting for 7.7% of annual issuance on average with a five-year run-rate of $102bn.

However, with the economic shutdown IG companies will continue to issue bonds for liquidity needs while others frontload as the market is wide open. M&A issuance totaled just $2.2bn in March and that may continue in April as global markets remain fragile, and T-Mobile/Sprint using a $23bn bridge loan for the April 1st closing with the IG bond refinancing delayed till when market conditions improve.

On the other hand, 1Q20 earnings-related blackouts will begin in the coming weeks, somewhat limiting the industrial pipeline as far as seasonality goes. As a result, BofA now looks for a wide range of $150-200bn of gross issuance in April. With $36.7bn of maturities in April and another $4.6bn of additional redemptions announced so far for a total of $41.3bn, the implied net issuance in April is $133.7bn.

If correct, total issuance in just the first 4 months of the year could reach a mindblowing $700BN, an unheard of number and one which means the Fed will very soon end up owning equity stakes in hundreds of bankrupt companies once its bonds are equitized as dozens of formerly IG companies are downgraded to junk, and then file for bankruptcy, convering the pre-petition debt into equity.

We, for one, can’t wait to see what the Fed will do when it ends up owning controlling post-petition equity stakes across countless US corporations.