“It’s Going To Bite Us” – Upside-Down Auto Loans Surge

March 3, 2023 in News by RBN Staff

source: zerohedge

Consumers face increasing financial difficulties due to high inflation, rising interest rates, maxed-out credit cards, lack of personal savings, and nearly two years of negative real wage growth, resulting in an emerging distress cycle for subprime auto loans.

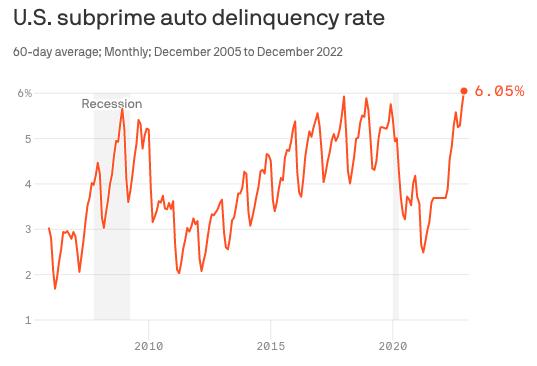

According to S&P Global, more than 6% of subprime auto loans were at least 60 days overdue in December, a more significant percentage than during the 2008-09 GFC.

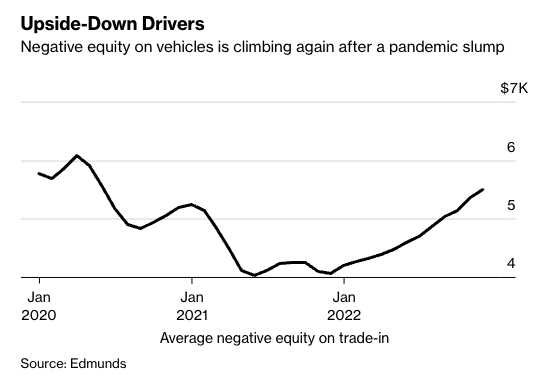

Bloomberg reported that auto dealers had noticed an alarming rise in customers who trade in their vehicles with negative equity of $10,000.

“As trade-in values begin to cool, each month more and more consumers will find themselves falling from positive to negative equity.

“Unless American car shoppers break their habit of buying again too soon, we’ll see the negative equity tide continue to rise,” Ivan Drury, director of insights at auto-market researcher Edmunds, said.

About one month ago, when discussing the “perfect storm” hitting the US auto market, we showed that according to Fitch, “More Americans Can’t Afford Their Car Payments Than During The Peak Of Financial Crisis“…

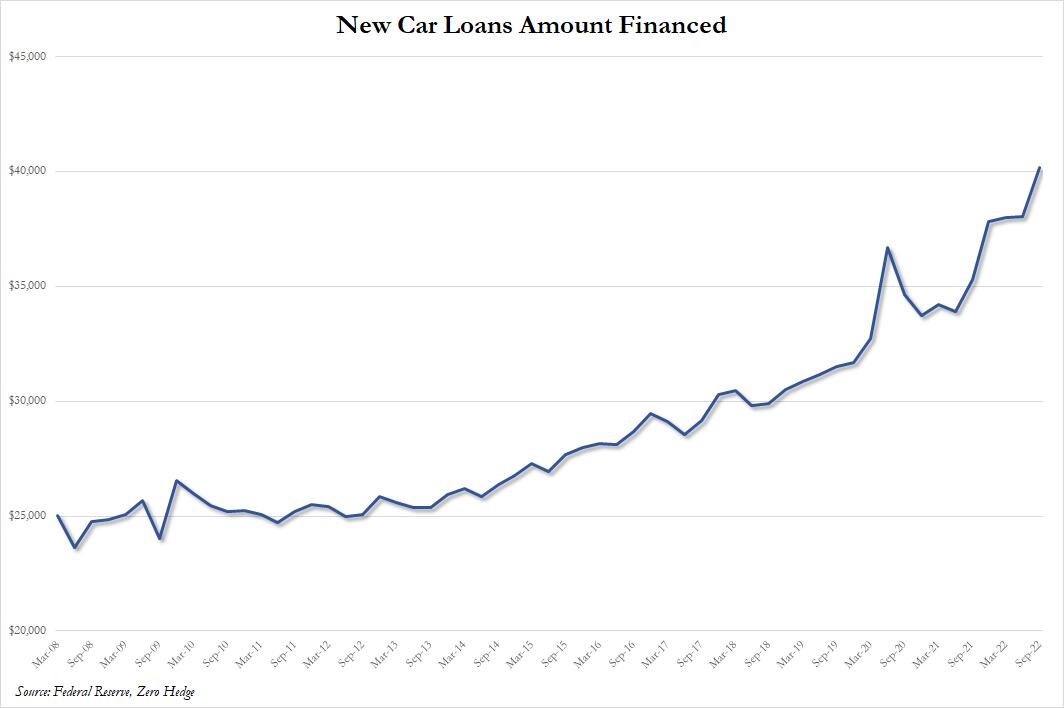

… which was to be expected: after all, the latest consumer credit report from the Fed revealed an exponential spike in the number of new car loans, which increased by more than $2,000 in one quarter, from just over $38,000 (a record) to $40,155 (a new record).

And purchasing a new car has become less feasible for the average person. Approximately two out of every 13 individuals are making monthly car payments of $1,000 or more. The average loan rate for new car loans just hit a 13-year high and will soon rise even higher.

Yet a giant wave of auto loan defaults among subprime Americans has yet to hit. Perhaps the negative-equity surge is the tipping point. Edmunds data shows average negative equity on trade-ins is approaching pandemic highs of $5,500.

“Because these car loans are generally unaffordable at the outset, that means that every month, borrowers are getting closer to the financial edge,” said Kathleen Engel, a law professor at Suffolk University.

Pete Kesterson, the general manager of a car dealership in Falls Church, Virginia, warned:

“It’s going to come, and it’s going to bite us,” referring to negative equity, which he believes will worsen.

“Now, we’re selling the cars for so much more, and financing for longer, at a much higher interest rate. There are some challenges coming down the pike.”

The rising delinquency rates for subprime auto loans are unexpectedly happening at the current record-low unemployment rates. Too many borrowers with low credit scores took on too much auto debt during Covid. Now the payback period has arrived.