Federal Reserve Playing Chicken With Financial Markets

September 27, 2022 in News by RBN Staff

source: zerohedge

Authored by ‘Monty Pelerin’ via EconomicNoise.com,

The game of chicken, learned by most teenagers, provides a reasonable description of current financial market conditions. The Federal Reserve is playing chicken with financial markets.

Usually the game of chicken determines a winner by whomever “blinks” first. In this case, there can be no winner, at least long-term. In order for the Fed to win, it must crash markets. In order for markets to win, they must call the Fed’s bluff.

The twist in this game of chicken is that the American people are barely aware of the game, but lose either way. If the Fed “wins,” inflation presumably comes back under control, but market values destroy the retirement assets and jobs of many. If markets win, inflation continues to destroy the standard of living of all.

Where Do We Stand Now?

Another rate hike of 0.75% this week was enacted by the Federal Reserve. The dollar, because of higher interest rates, is strong against other currencies, but financial assets are weakening. This site has been tracking four key asset classes. Their performance is summarized below:

Everything was down (red) this week and seriously so! Since the closing prices of July 26 (the day before the first of three rate increases), all tracked securities are negative and becoming increasingly so. Markets reluctantly believe that Powell means what he says.

Hit hardest was TLT, the 20-year Treasury Bond ETF (bond prices move inversely to interest rates). Suffering the least (although not by much) was GLD, considered a hedge against inflation. (That is not unusual at this stage of an inflation battle because of the strengthening of the dollar versus competing currencies.)

Do Markets Fully Believe Powell?

When Powell began hiking rates, he had little credibility. As the rate hikes continued, credibility improved, but still does not reflect his promises. Markets seem to believe what he has done, but not what he has promised.

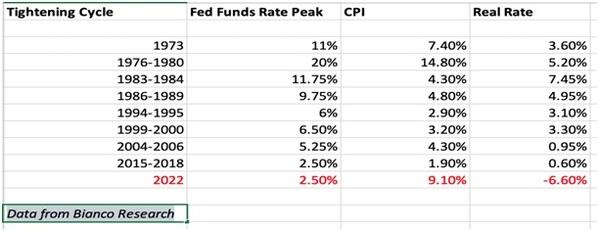

This presents a danger, because markets do not value based on history but on expectations. As yet, they do not believe Powell’s promise to stop inflation! This opinion is derived from prior battles with inflation as summarized in this table:

From this information, if the Fed is as serious as Powell claims, they have just begun rate hikes! In all instances above, the real rate of interest (defined as the interest rate minus the inflation rate) had to go positive to stop inflation. In most cases, a real rate of at least 3% was required. Assuming inflation is 8 or 9% today, that means the Fed would have to raise interest rates to 11 or 12%! Interest rate expectations like these are not reflected in current market valuations. Nor need they be for markets to react to them coming! If Powell were entirely credible in his promises, markets likely would be 50% or lower from here!

That they are not suggests Powell is still incredible in his claims/threats. Current market valuations reflect Fed actions, not intentions. They reflect what has happened, but not what was promised!

Markets are anticipatory and their price levels are determined by expectations, not history. Powell’s promises and current market values are inconsistent with one another. Does Powell blink? Will market participants, at some point, suddenly and violently believe him? These are the critical but unknowable questions.

Each rate hike boosts Powell’s credibility (at least with respect to his intent to halt inflation). He does not have to get to his implied stopping point for market valuations to reflect his threats, but he must get to this point if he intends to control inflation!

At some point, markets will believe or disbelieve Powell. This shift in beliefs will be sudden and herd-like. You do not want to be in the path of this herd reaction! Widespread belief in his intentions likely produces another 50% movement down from current valuations. Disbelief does not produce a market rally because the existing problems are still unsolved!

Each rate hike influences more investors to believe Powell. Another one or two increases could cause markets to crash well in advance of Powell’s end point. Markets could crash even before another rate increase. Information and how it is processed is impossible to project. However, herd-like reactions, rightly or wrongly, can result. These reactions typically “anticipate” future information. Market “stampedes” are not unusual and always damaging if you are in the wrong place!

More people believed in Powell’s intentions after his July 27 rate hike. And more have come to that conclusion with the two subsequent rate increases. Market performance this week suggests a sizeable increase in believers. Sentiment shifts like these occur in unpredictable fashion. They also are capable of producing herd-like movements in buying/selling. Being on the wrong side of the herd is always painful.

Markets are likely to continue to decline for two reasons:

- More people see the losses in their personal portfolios and want to stop the pain.

- More investors decide that Powell’s fight is credible.

We lived through several years of “panic buying.” We are near or already in a period that likely will be referred to as “panic selling.”

Up until now, markets appeared to be reacting to events rather than anticipating them and reacting to expectations. If markets finally agree with the Fed’s stated intentions, another 50% drop or more from these levels could easily occur. We could be very close to a selling panic!

Is Powell for real? I don’t know! I know there is something strange regarding his recent behavior (as mentioned in a prior post). Michael Snyder ends a recent piece with this:

[W]e are eventually headed for a meltdown of epic proportions.

But instead of working to prevent a historic crisis, the Federal Reserve is actually encouraging one.

The American people deserve some answers, because there is something about all of this that really stinks.

An interesting discussion on CNBC business provides a different, although not too dissimilar outlook. Perhaps there is more going on than is obvious. However, that subject is a different post.